The WaMu Story

Home

Saga of $4B

Economics

JPM Benefits

Court

People

Securities

WaMuSubsidiaries

WaMuEquityGroup

Contact

The Speaker is Charlie Scharf, Chief Executive Officer of Retail Financial Services, speaking at a JPMorgan Shareholders Meeting, about the WaMu Seizure.

It's about 2 minutes long.

It should automatically play, but if not here's a link: charlie

Charlie Scharf Speaking:

"Great brands take a long time to build" - Like the WaMu Brand for instance???

Please Register your Shares: WaMu Equity Group

Case Numbers:

Ch11: 08-12229

Adversary against JPM/FDIC: 09-50934

Bottom Line: WaMu was RAPED on her Birthday, by the COLLUSION between JPMorgan, the FDIC, the OTS, the courts, the SEC and persons in government.

Note

that many documents linked to in this page have been removed by people involved and unknown, in order to hide the

truth.

Note also the amount paid for WaMu: $1889M. $1M more than the year she

was born: 1888. Guess they didn't pick the number out of a hat did they?

Latest Development 6-3-2009: WMI files Counter Claims against JPM for Billions of dollars: WMI Counter Claims

What follows is a detailed timeline of the events surrounding the seizure of Washington Mutual Bank. We have a condensed version here: The Short Version.

Calendar of Important Dates: http://www.my.calendars.net/wmi

5-20-2009: WMI moves

to investigate JP Morgan!! Seeks $Billions in damages.

Phrases like 'far below market value', 'premeditated plan', 'designed

to damage', 'purchase...on the cheap', 'wrongful conduct',

'sham negotiations', 'misusing confidential information', 'violation of

confidentiality agreement', 'unfair advantage', and 'fire sale prices'

are in the court motion: CNBC

Story

WMI is also suing JPMorgan for return of their $4Billion deposit.

Washington Mutual Inc has filed suit against the FDIC, and seeks damages of approx $40 Billion: WMI vs FDIC Filed Document.

Behind the scenes. The havoc wreaked by some very powerful men: The Goldman Conspiracy:

Latest Monthly Operating Report:: April 2009 Operating Report

From the book 'House Of Cards: A Tale Of Hubris And Wretched Excess On Wall Street' by Cohan, William D.

This book includes proof that Chase/JP Morgan acted in concert with the US Treasury and the Fed to acquire Bear Stearns for a pittance which then set the stage for a repeat-performance when Chase/JP Morgan was allowed to buy Washington Mutual banks at a fire sale price.

Here is a small peek into the inner workings that brought WaMu down:

A final decision had just been made by the US Treasury, i.e., Hank Paulson, in tandem with the Fed and major firms on Wall Street, that there would be no bailout of Lehman Brothers and that Lehman Brothers would be forced into bankruptcy.

After Thain, Paulson and Geithner had left the New York Fed Sunday morning, the following exchange ensued, according to several sources that were there. John Mack, the CEO of Morgan Stanley, spoke up. 'Maybe we should let Merrill [Lynch] go down, too. he said.

Aghast, JPMorgan Chase's [Jamie] Dimon pointed out how shortsighted that was of Mack because Morgan Stanley might be the next firm that counterparties lost faith in. 'John, if we do that, how many hours do you think it would be before Fidelity would call you up and tell you it was no longer willing to roll your paper?'

Dimon's comment quieted Mack. 'We thought Mack said that because he might

be buying Merrill,' someone who heard Mack's statement said, and wanted

to buy the firm on the cheap. (Mack denied he made the comment through

a spokesman. A spokesman for Dimon said Dimon did not remember having

the conversation with Mack.)

The Wamu Story

Washington Mutual Bank, or WaMu, as it was known

by its customers and employees, was seized on Thursday, September 25,

2008. The OTS intended to seize them on Friday, but the schedule was moved

up one day when a media leak threatened to expose the seizure.

This is the story of what happened, and when,

as well as some factors that affected the demise and sale of the bank.

It should be noted that Washington Mutual Bank (WMB) was the largest thrift

in the United States, and one of its largest banks. The seizure and sale

were conducted in secret while Washington Mutual Bank was still well capitalized,

liquid, while TARP was pending, and in fact at the same time WaMu was

seeking bids to sell itself.

Washington Mutual Bank (WMB) was a subsidiary of Washington

Mutual Inc. (WMI) Washington Mutual

Inc had many other subsidiaries before the seizure and sale by the OTS

and the FDIC. They had many less

subsidiaries after that transaction-- some that may have not been associated

with or subsidiaries of the bank (WMB).

http://www.thewamustory.com/subsb4.htm

Subsidiaries Post Seizure

See pg.22

http://www.kccllc.net/documents/0812229/0812229081126000000000005.pdf

Washington Mutual had $307 Billion in

assets, $188B in deposits, 2239 branches, 4,932 owned and branded ATMs,

and 43,198 employees at the time of seizure.

They had multiple subsidiaries that were sold as well. The FDIC brokered the “sale” for $1,888 Million.

Washington Mutual began after the “Seattle Fire” of 1889 was seized

on its 119th Birthday.

The

FDIC decided that $1,888 Million was a just and fair price for the bank. It is interesting to note that the auction

offer presented by the FDIC permitted banks to bid $0.0

for the bank, and also totally disregarded the stockholders and bondholders,

as well as other liabilities of the bank.

The FDIC required only the administrative costs for the transaction,

and held the bank for only a few hours before ownership was transferred

to JPMorgan. Washington

Mutual Bank was forced to file Chapter 11 the following day. They lost $26 Billion in stock of WAMU (WMB)

due to the bank seizure.

The recent declines in the stock market are

well known, but few people realize that WaMu may have been the straw that

broke the camel's back. This seizure impacted not just Washington Mutual

Inc investors, but all types of investments in all US stock markets. Shock

waves have cascaded throughout stock markets worldwide. This leads one

to question whether Washington Mutual Bank should have been seized that

September evening. The sale of WAMU, for a fraction of its worth, was

conducted without regard for the bondholders or shareholders of the bank,

much less for the effects to the confidence in our stock markets and our

government in general.

Should WaMu have been seized, that fateful day?

Did the regulatory bodies

overseeing WaMu do their jobs properly?

You be the judge.

In April, 2008, JPM

tried to buy Washington Mutual. They

had long coveted the thrift for its many branches in markets where they

had none and wanted to expand. The

price of expanding by themselves, without buying Washington Mutual, was

cost-prohibitive. Washington Mutual considered the $8 per share offer

from JPMorgan too little for the expansive bank with $307B in assets, $188B in deposits,

2239 branches, 4,932 owned and branded ATMs, and 43,198 employees.

JPMorgans offer was

rebuffed and Washington Mutual chose to enter a contract with TPG and

several investors instead, for a $7 Billion Capital injection. David Bonderman

heads TPG, a company known for its talent in identifying and maximizing

investment opportunities. Bonderman

had been on the Washington Mutual Board of Directors previously and rejoined

the board as part of their agreement.

http://www.tradingmarkets.com/.site/news/BREAKING%20NEWS/1332198/

http://www.tpg.com/about/index.html

“Two months before Washington Mutual

failed, Treasury Secretary Henry Paulson warned then-CEO Kerry Killinger

that he ought to sell the Seattle-based thrift before it deteriorated

further. ‘Paulson said, 'You should

have sold to JPMorgan Chase in the spring, and you should do so now. Things

could get a lot more difficult for you,' said one of several current and

former high-ranking WaMu executives familiar with details of the call.”

07/15/08--SEC

Enhances Investor Protections Against Naked Short Selling

That

makes it sound like they were doing their job doesn’t it? Unfortunately it was well known by hedge funds and other “shorters”

that the naked short selling ban was not enforced.

Naked

short selling of Washington Mutual continued to damage Washington Mutual

severely and although it is illegal, the SEC did nothing to stop it.

WaMu was not put on the list of banks that were not to be shorted. WaMu

CEO Killinger specifically asked for WaMu to be added to the list but

was refused. The Short ban notice announcement

on 15 July by the SEC was to be effective the 21st. On July 17, Killinger, the CEO, sent a FAX

transmittal, requesting to be added to the “no short” list and was refused.

It is interesting to note the fax, which was received on the 17th

was logged in as received 8:40pm on the 22nd by the "Chairman's Correspondence

Unit".

http://www.sec.gov/news/press/2008/2008-143.htm

http://www.sec.gov/rules/other/2008/34-58166.pdf

http://edgar.sec.gov/comments/s7-20-08/s72008-553.pdf

The American Bankers Association, representing the interest of 8,500 banks,

said in a letter to the SEC that it fears short sellers will now concentrate

their efforts on banks that are not covered by the emergency order. They

asked that the order be expanded to include stocks of all banks and bank

holding companies. This request

was also ignored.

http://www.mortgagenewsdaily.com/7222008_Short_Sell_Banks.asp

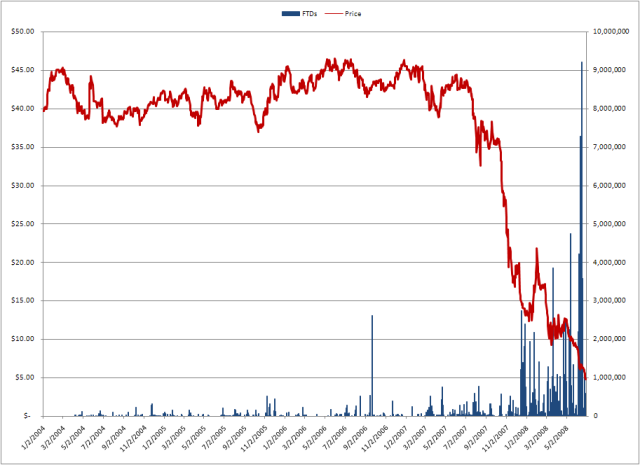

Evidence of Damage Caused by Naked Short Selling: WAMU Stock

Price vs. Failure to Deliver (FTD) of Securities

http://www.deepcapture.com/wp-content/uploads/2008/09/wamu.png

{kind=link}

September 29, 2008

American Banker

magazine cites that the OTS did not want to seize the bank but the FDIC

pressured them into it.

http://tinyurl.com/amr3jy

It has been widely discussed that the FDIC was under funded to cover the

amount of deposits they had to insure, and that the FDIC and OTS had differing

opinions about whether WAMU should be seized. The FDIC feared depletion

of its reserves and they expected other bank failures. Congress had not

increased its ability to raise premiums for many years, and indeed no

bank premiums were collected from 1996 to 2006, as the FDIC was at its

maximum threshold as required by law. They have since increased their

premiums.

It is interesting to note however, the FDIC did have the ability to borrow

$30 Billion from the Treasury at the time. It is not clear why they did

not use their discretionary power to support the one of the largest banks

in the country, at least on a temporary basis. The bank had access to

$54 Billion of liquidity at that time--$4 Billion was on deposit at Washington

Mutual Bank and another $50 Billion was available, assumedly from the

secondary window at the Federal Reserve in San Francisco.

http://www.nypost.com/seven/09262008/business/capitol_wamu_ve_130800.htm

http://www.kccllc.net/documents/0812229/0812229081009000000000002.pdf

While all of this was happening the Economic Stabilization Act was being

discussed in Congress. While there was no question that TARP, as it has

come to be known, would eventually pass, there were arguments over many

details to be worked out. The bailout would have alleviated the banks

difficulties, at least in the short term, until a proper sale could be

arranged, rather than a "fire sale" which ultimately gave the

bank away for far less than fair value. The fact that the bailout was

pending meant banks were hesitant to bid due to the uncertainty; this

has been well documented in multiple news articles.

http://files.ots.treas.gov/73002.pdf

http://ori.msnbc.msn.com/id/26859148/

NOTE: There is no record of any document wherein WaMu

was required to raise additional capital, or improve its liquidity.

On 09/25/08 the OTS released a press release and recording

about the seizure of Washington Mutual...it notes they were well-capitalized

at the time of the seizure.

http://tinyurl.com/abm8gf

OTS Enforcement Actions noted on this report.

-- October 17, 2007 – Issued a Cease and Desist Order related to deficiencies

in Bank

Secrecy Act/Anti-Money Laundering (BSA/AML) programs

-- October 17, 2007 – Assessed Civil Money Penalties (CMPs) related to

violation of

flood insurance regulations

-- November 14, 2007 – Initiated a formal examination of the appraisal

process to

assess the validity of a complaint filed by the New York Attorney General’s

(NYAG) Office

-- February 27, 2008 – Issued overall composite ratings downgrade and

received a

Board resolution in response to the supervisory action

-- June 30, 2008 – Initiated discussions about Memorandums of Understanding

with

WMI and WMB (Washington Mutual Bank)

-- September 7, 2008 - Issued Memorandums of Understanding to WMI and

WMB

-- September 18, 2008 – Issued overall composite ratings downgrade

OTS Press release

recording

Discusses the bank seizure.

http://files.ots.treas.gov/4811117.mp3

Sept 8, 2008. WaMu said that it has entered into a memorandum of understanding

with the Office of Thrift Supervision concerning aspects of its operations.

WaMu committed to provide the OTS with an updated, multi-year business

plan and forecast for its earnings, asset quality, and capital and business

segment performance. The plan did not require the company to raise capital

or increase liquidity, WaMu said. (This plan was approved by the OTS)

http://www.usatoday.com/money/economy/2008-09-08-3382390904_x.htm

09/11/08: WaMu provides an Update on Expectations for Third Quarter Performance

and notes the company continues to maintain a strong liquidity position

with approximately $50 billion of liquidity from reliable funding sources.

“The company's tier 1 leverage and total risk-based capital ratios at

June 30, 2008 were 7.76%, and 13.93%, respectively, which were significantly

above the regulatory requirements for well capitalized institutions. The

company expects both ratios to remain significantly above the levels for

well-capitalized institutions at the end of the third quarter.”

(newsroom.wamu.com)

http://newsroom.wamu.com/phoenix.zhtml?c=189529&p=irol-newsArticle_Print&ID=1196448&highlight=

http://www.reuters.com/article/pressRelease/idUS238676+11-Sep-2008+BW20080911

12/31/08: OTS press release regarding TARP after they saw

what mayhem the seizure of Washington Mutual caused.

http://www.ustreas.gov/press/releases/reports/0010208%20sect%20102.pdf

It

is interesting to note that the West Coast Regional Director, Darrel Dochow,

was transferred after it was discovered there were irregularities in bookkeeping

methods, which were approved by Dochow, in the Indy Mac failure.

It has been also revealed that he permitted bookkeeping irregularities

with 4 other banks in his region. The

other banks have not been named. Dochow

had also been implicated in oversight failures in the Savings and Loan

crisis in the 1980’s and 1990’s. Dochow

was demoted after that, but was later promoted again to West Coast Regional

Director. He was transferred after the Indy Mac irregularities

were made public and he later retired.

http://www.nytimes.com/2008/12/23/business/23thrift.html?_r=1&ref=business

FDIC

Actions that adversely affected the sale and auction of Washington Mutual

09/23/08: FDIC auction "offer" -- essentially says that the

bidders can have the bank for nothing as long as they pay the administrative

costs of the transaction. (which are left blank)

It also says they can have any assets, whether they are on the

banks books or not (this info is on page one).

http://wmish.com/docs/gib/Washington_Mutual_Bank_Closing_Book.pdf

Sheila Bair said that the Washington Mutual seizure was done at no cost

to the taxpayers, but what were the administrative costs? That part of

the agreement was left blank. The shareholders and bondholders who lost

as much as $30 Billion were not considered, nor were the corporations,

Pension plans, or other institutions who owned (at that time) approximately

68% of Washington Mutual Common Stock.

(E-trade). Retirements for many people were wiped out

either directly by the loss of value in Washington Mutual Stock, or indirectly

through the loss in their Pension plans, 401K’s and the general market

panic that ensued. There is also a human cost; JPM has announced layoffs

of 9200 WaMu employees with plans to cut an additional 2800 by attrition. It has recently been noted in the news that

JPMorgan has made plans to outsource many jobs in their organization.

All the following documents regarding the FDIC auction are posted at http://wmish.com/docs/ and were

supplied by the FDIC via FOIA (Freedom of Information Act)

FDIC

sends out “official” bid notice. Date of fax –Sept 24, 2008.

Excerpt:

“5. Definitive Documents. Each Potential Acquirer's bid(s) should be based

upon the relevant transactions described in the Legal Documents and these

Instructions. Each should note that the transactions are merely summarized

herein and the Legal Documents are much more detailed. The Legal Documents

will govern the transaction regardless of the contents of these Instructions

and any other written or oral material or communication.”

http://wmish.com/docs/gib/WaMuBidInstructions.pdf

JPMorgan bid for WAMU…NOTE: The details of the bid are

redacted.

http://wmish.com/docs/JPMCoverLetter.pdf

Washington Mutual Bank Closing book Sept 25, 2008: Date of seizure.

Excerpt:

“The bid for alternatives 1, 2, or 3 must be at least the FDIC's administrative

costs of the closing equal to $_________________ (amount to be provided).

Assets Purchased: The Assuming Bank will purchase all assets whether or

not on the books of the Bank, except for those that are specifically excluded

under Article III of the Whole Bank agreement. In general, all assets

are acquired at book value with the exception of securities which are

purchased at fair market value.”

http://wmish.com/docs/gib/Washington_Mutual_Bank_Closing_Book.pdf

Of note, there was another bid for the bank. The FDIC will not release

any information on that bid. Another FOIA request confirmed the bidder

as Citigroup, but their bid was deemed "nonconforming" and the

information was so heavily redacted that it was nearly a black page.

http://i34.tinypic.com/73dxg0.jpg

Also of note, banks were quoted as saying they would not bid on WAMU until

they saw what would happen with TARP. Congress was debating the issues

and it was expected to pass at any time. TARP passed 8 days after WAMU

was seized.

Four banks submitted their plans by the Wednesday due date, and the same

day JPMorgan was notified it had won. The FDIC declined to name the other

participating banks.

http://www.reuters.com/article/etfNews/idUSN2631577020080926

The FDIC updated their billing process on Sep 23rd, the same

day they secretly put WAMU on the auction block. The seizure was later

moved up one day due to a “leak”-- the secret auction was no longer a

secret and had been leaked to the press. Though widely discussed in the

press, the source of the leak has not been identified.

http://www.fdicig.gov/reports08/08-018.pdf

FDIC Purchase and Assumption Agreement

http://www.fdic.gov/about/freedom/Washington_Mutual_P_and_A.pdf

NOTE: It cites Schedule 3.1a as a list of the assets to be purchased.

After someone wrote the FDIC wanting a copy of that list, they then changed

the FDIC website indicating that it was a scrivener’s error and no 3.1a

document exists. It appears there is NO LIST of what was included in the

purchase.

Statement

of Assets & Liabilities in Liquidation (unaudited) FDIC document

It should be noted that the value placed on Washington Mutual Bank varies

widely, depending on the source. The figures cited by the FDIC are noted

to be "unaudited".

{kind=link}

http://wmish.com/docs/WaMuReceivershipFinancialStatements(unaudited)thru123108.pdf

JPMorgan

divulges they knew about the seizure Sep 19th, and it actually

sounds like the “deal was done” before the auction began.

Investor’s

Day 26 FEB 2009 08:30

Charlie Scharf (JPMorgan) said, at their Investor’s Day Conference, they

were notified about the bank seizure on Sept. 19, 2008. Fast forward to

3 hours 14 minutes to hear the following excerpt:

"We did a lot of work over a long period of time...really analyzing

the company, and then when the deal got done, it happened very very quickly.

Got

the call from the FDIC on a Friday (9-19), they came to meet with us on

a Monday (9-22), the deal was announced Thursday night (9-25). the deal

was announced Thursday night, that night as Mike mentioned Rick raised $11B of capital, and then Friday morning, Todd

was in California and Gordon was in California, different places cause

uh Irvine vs. San Fran.

I

was out in ah Seattle, Frank came out to Seattle, J (Dimon) was out in

Seattle, the place…you know it was ours the next day...very, you know

non traditional transaction with immediate ownership"..."the

business was seized by the FDIC" -- Charlie Scharf, Chief Executive

Officer of Retail Financial Services.

Charlie Scharf Speaking:

A little known fact is that Washington Mutual had $50 Billion cash available

from the secondary Fed Reserve Window in San Francisco. One must wonder

whether the OTS and the FDIC knew about this. It is apparent the FDIC

did not know about the $4 Billion dollar deposit, as they later tried

to claim it in bankruptcy court. JPM

also tried to claim this money in court. The court determined the money

belonged to the parent company, Washington Mutual Inc. (WMI).

http://www.kccllc.net/documents/0812229/0812229081009000000000002.pdf

It appears JPMorgan may have known well in advance of the plans for seizure

(by some reports three weeks in advance). It is unknown whether the other

banks were also unofficially informed of the seizure, well in advance. Was the auction a fair playing field? Did all

the bidders have the same information JPMorgan had?

Washington Mutual was not aware of these backroom discussions

between JPM and the FDIC. In fact, Washington Mutual, through Goldman

Sachs, was trying to sell the bank on the open market to those very same

banks, but curiously their attempt drew no bidders.

Why would a bank bid openly with Washington Mutual when they

knew the FDIC was offering a deal, behind Washington Mutuals back for

only the choicest assets instead of the entire bank? The FDIC was offering a much better deal, then Washington Mutual

was able to offer, you see the FDIC offered the bank for the price of

$00.00. Their behind the scenes

discussions interfered with the banks ability to sell itself.

Did JPM know three weeks prior to Sept 25 of a possible FDIC seizure?

Was the bidding process fair and impartial? That is an issue for a Congressional

Hearing to decide. The entire matter is currently under a clandestine

investigation. Many shareholders

have contacted their Congressional Representatives requesting an open

Congressional Hearing on this matter.

In most cases they have received no response from Congress.

Sheila Bair said, shortly after the seizure of Washington

Mutual, the seizure was stepped up due to a leak. “Washington Mutual was on the radar for some time, said Bair,

who noted that the timetable for the seizure was bumped up due to a potential

media leak. She added that all deposits, both insured and uninsured are

covered.”

http://www.economicnews.ca/cepnews/wire/article/126804

But here she says it was stepped up due to its deteriorating

condition. She said that “the bank’s rapidly

deteriorating condition prompted regulators to seize it Thursday, and

not on a Friday as is typical for bank closures. “ Which is it Ms. Bair? On the date of seizure (earlier in the day

than the bank was seized), CNBC aired a short news clip about a bank run

they identified as Washington Mutual, and then “broke” for commercial. When they came back online they noted that

the previous story was inaccurate, and the bank run was at a different

bank (Indy Mac?).

http://www.nytimes.com/2008/09/26/business/26wamu.html?_r=1&ref=us

News stories often report that Washington Mutual was seized

after withdrawals of $16.7 Billion over a nine day period which began

on Sep 15th. As we now know, there were plans to seize Washington

Mutual before the 25th. In

fact, JPMorgan was notified Sept 19th about the seizure, and

indeed knew about the prospects for seizure three weeks in advance. No information has been released regarding

the situation at the time the OTS began making plans to seize the institution.

http://www.huffingtonpost.com/2008/09/25/jp-morgan-to-buy-wamu-ass_n_129451.html

Later, Paul Kanjorski stated on national television that there was a $550 Billion

drawdown in the market at this time.

What effect did this have on the seizure of Washington Mutual?

The “Economic

Meltdown”

09/18/08: It has recently come to light that on the 18th of September

there was a 550 Billion dollar drawn down on money market funds during

a 2 hour period, and there was panic among regulators

(Frontline--PBS). This indicates that most, if not all, banks

were under significant pressure at that time. There is much discussion

about the veracity of this statement by Paul Kanjorski.

http://tinyurl.com/cur3nl

http://online.wsj.com/article/SB122869788400386907.html?mod=todays_us_page_one

Why was Washington Mutual singled out when this draw down was occurring

at all banks? There was a systemic country wide financial meltdown; why

was WAMU seized? Washington Mutual was liquid and well capitalized. The

seizure was unjustified, premature, and unwarranted.

The FDIC arranged a similar transaction in the case of Citigroup's acquisition

of Wachovia for $2.1 billion. It was in the form of a forced sale, under

the threat of seizure. The agreement reached would have required federal

assistance to mitigate risk to Citigroup. However, Wells Fargo offered

$15 billion to purchase Wachovia outright shortly thereafter despite Citi's

signed deal. A legal battle ensued, the FDIC maintained

that it stood behind Citigroup and the deal it had brokered, but Wells

Fargo was the eventual victor due to their superior offer.

http://online.wsj.com/article/SB122303190029501925.html

http://northcoastinvestmentresearch.wordpress.com/tag/wfc/

Perhaps the differentiating factor was the fact that the sale of Wachovia

was done publicly, over a period of a week or more, rather than secretly

over a period of hours, as the WAMU "deal" had been completed.

Stock market charts show that the day following the seizure of WAMU, the

markets took a nosedive. This is thought to be because investors felt

they could no longer trust the government, since they had become erratic

in their treatment of the banking crisis. The OTS/FDIC caused the very

thing it is supposed to prevent: a bank panic. The premature seizure destroyed

the value of WaMu's bondholders and stockholders, at the same time destroying

confidence in the market. Why invest in any publicly traded company if

the government can arbitrarily seize your interest, leaving you nothing,

or perhaps pennies on the dollar?

Note the market performance since the 09/25/2008 seizure:

How J.P. Morgan

Raised $11.5 Billion in 24 Hours

http://blogs.wsj.com/deals/2008/09/29/how-jp-morgan-raised-115-billion-in-24-hours/

Three weeks before JPMorgan bought WaMu’s deposits for $1.9 billion, officials

at the Federal Deposit Insurance Corporation had called JPMorgan to say

that the FDIC was carefully monitoring WaMu and that a seizure of its

assets was likely. There have been no news articles indicating that the

other banks were notified at that time.

http://blogs.wsj.com/deals/2008/09/29/how-jp-morgan-raised-115-billion-in-24-hours/

Since the seizure, JPMorgan and the FDIC have challenged Washington Mutual

Inc (the Holding Company that owned WMB) on tax benefits of writing off

its losses prior to the seizure.

http://www.reuters.com/article/governmentFilingsNews/idUSN3025944620081030

01/22/09: JPMorgan objects to having to show what they bought (file claim)

by 3/31/09. That may be because

they can't; there is no list in the Purchase and Assumption Agreement

(3.1a), although the purchase agreement cites there should be. The purchase

agreement is incomplete. JPMorgan objected to having to show any claim

by the claim filing deadline. Their objection was overruled by Judge Walrath,

the judge presiding over the bankruptcy case.

http://www.kccllc.net/documents/0812229/0812229090122000000000001.pdf

02/05/09: Weil and Gotshal have filed a claim against the FDIC (December

30, 2008). WMI was given $0.00

for the bank, despite a book value well over $20 billion at the time of

seizure. The FDIC failed to get a reasonable price, even though they are

required by law to maximize the return on the assets seized as well as

to minimize the impact to the FDIC fund.

There are many differing opinions on what the value of the bank

was, but of the sources we could find, none felt the bank was worth a

mere $1.9 Billion. JPMorgan got the bank at a substantial discount, as

they have documented well in their SEC filings. They even booked a $1.9

Billion gain the next quarter – not a bad return for three months. The

FDIC also gave JPMorgan many subsidiaries.

Some of those subsidiaries may not have been on the banks books,

and in fact may have belonged to the parent holding company, Washington

Mutual Inc (WMI). WMI filed a claim against the FDIC's receivership

on 12/30/2008. According to a

Weil & Gotshal representative, the claim submitted to the FDIC was

denied in late January 2009.

Page 9

http://www.kccllc.net/documents/0812229/0812229090205000000000005.pdf

SEC did not do its job; illegal short selling damaged

WaMu

7/21/08: SEC bans “naked” short selling in certain

financial stocks. Washington Mutual is not included on the list.

http://www.mortgagenewsdaily.com/7222008_Short_Sell_Banks.asp

9/17/08: SEC bans “naked” short selling of all

stocks.

http://www.sec.gov/rules/other/2008/34-58572.pdf

9/18/08: SEC bans short selling of 799 financial companies, including

Washington Mutual.

General resource on the surrounding economic legislation and SEC and FED

actions:

http://www.philadelphiafed.org/payment-cards-center/legislative-update/2008/3q/

Did

the FDIC do their job properly after the seizure of Washington Mutual?

Sheila Bair, in a 60 Minutes episode which aired on March 8, 2009, said

that the FDIC did not shutter big banks. Washington Mutual was a big bank

and the fallout from its seizure was widely felt in the US markets and

indeed around the world. Stockholders were essentially wiped out in this

seizure, due to the fact that the FDIC permitted the deal to be written

with no regard to provisions for the stockholders. Although it is unknown

exactly what the total losses were, it is estimated it could be as high

as $30 billion. Many of these stockholders were Pension Funds, large institutions,

as well as individuals 401K's, IRA's and other private accounts. The question

at this point is whether the FDIC acted appropriately in only getting

1.9 Billion dollars, and allowing the stockholders to be left out of the

transaction, and completely out in the cold. Many institutions were severely

impacted by the sale agreement the FDIC arranged. The sale agreement had

far reaching, adverse effects both on portfolios and the market in general.

9-17-08: A WSJ article states that WaMu has hired Goldman Sachs to find

a buyer of the bank.

9-18-08: WaMu's rating slips to a 4 and is placed on the FDIC's watch

list, a fact kept secret at the time to prevent a self-fulfilling run

on the bank. A 4 rating reflects financial, operational or managerial

weaknesses that threaten a bank's financial viability.

9-19-08, Friday: FDIC talks with JPM about WaMu. (From JPM presentation

on 2-26-09)

9-22-08, Monday: FDIC meets with JPM. (From JPM presentation)

9-24-08, Wednesday: 4 banks reportedly submitted bids/plans to FDIC by

the deadline set by the FDIC:

FDIC Chairman Sheila Bair told reporters on Thursday that after an open

process to find a buyer failed, the agency turned to its secretive auction

process in which bidders place their offers on a secured website. The

auction turned out to be not so secret when a media leak prompted early

seizure of the bank. The "leak" has not been identified.

Which other organizations bid for WaMu, and the contents of those bids,

have not been revealed by the FDIC. Here is an abbreviated timeline of

what happened.

9-24-08, Wednesday 6:44PM: JPM submits bid to FDIC of $1,888M

9-25-08, Thursday: OTS seizes WaMu and gives it to FDIC

9-26-08, Friday: FDIC sells WaMu to JPM for $1,888,000,000.

2-26-09: JPM states that the WaMu transaction was 'very non-traditional'.

(From shareholder presentation).

Did the FDIC

do a fair and impartial auction?

Were all banks given the same information at the same time? By some reports

JPMorgan knew of the auction 3 weeks prior. Did other banks have that

same advantage? JPM was notified on Friday, 9-19 that they would get the

bank. That was days before the auction officially began. Of note, JPMorgan

raised approximately $11 Billion for the purchase, yet they managed to

buy the bank for a mere $1.9 Billion. The auction permitted the banks

to bid $0 for the bank, and totally disregard the stockholders and bondholders.

Although stockholders and bondholders are not technically the FDIC's responsibility,

was it wise or fair to totally disregard the interests of these stakeholders?

FDIC regulations as quoted from their official website:

http://www.fdic.gov/regulations/laws/rules/1000-1220.html#1000sec.11d

12 U.S.C. 1821(d)

13) ADDITIONAL RIGHTS AND DUTIES.--

(E) DISPOSITION OF ASSETS.--

(i) maximizes the net present value return from the sale or disposition

of such assets

(ii) minimizes the amount of any loss realized in the resolution of cases

(iii) ensures adequate competition and fair and consistent treatment of

offerors

JPMORGAN CHASE Acquires the deposits, assets and certain liabilities of

WASHINGTON MUTUAL’S banking operations

http://tinyurl.com/aq3v4w

JPM's Bid For WaMu via FOIA Request

http://wmish.com/docs/gib/JPMorgan_Bid_September_24_2008.pdf

What Did JPM Purchase?

It is still not clear exactly what JPM purchased from the FDIC on 09/25/08,

because their Purchase and Assumption agreement didn't disclose exactly

what was sold, other than as stated in paragraph 3.1, "...all of

the assets (real, personal and mixed, wherever located and however acquired)

including all subsidiaries, joint ventures, partnerships, and any and

all other business combinations or arrangements, whether active, inactive,

dissolved or terminated, of the Failed Bank whether or not reflected on

the books of the Failed Bank as of Bank Closing." This statement

clearly did not address the possibility of joint ownership of assets by

Washington Mutual Bank (WMB) and their holding company, Washington Mutual

Inc. (WMI). The seizure of assets which were not on WMB's books leaves

open the real possibility that some of those assets actually belonged

either solely to WMI or were owned jointly and as such were not rightfully

seized.

It appears that that Schedule 3.1a had been intended to be more specific

regarding the assets sold. This section is missing, despite being referenced

repeatedly in the version of the document posted initially on the FDIC's

website.

http://www.fdic.gov/about/freedom/Washington_Mutual_P_and_A.pdf

An early rough draft was obtained by FOIA request:

http://wmish.com/docs/gib/Washington_Mutual_Bank_Closing_Book.pdf

What Did JPM Gain?

JPM had long coveted WaMu's West coast branch network, and had earlier

offered $8 per common share for the entire company, an offer that would

have assumed all debt and preferred stock of both WMB and WMI. It was

rebuffed at the time for being too low; it was less than WMI common stock's

market price at that time.

Through the seizure and acquisition,

JPM expanded its' banking footprint into states with little Chase coverage.

These include Washington, Oregon, California, and Florida. Along with

$307B in assets they acquired $188B in deposits, 2239 branches, 4,932

owned and branded ATMs, and 43,198 employees.

They were also given the ability to return any branches they

didn't want to the FDIC. JPM has indicated it would lay off 9,200 employees

and recently indicated they would cut another 2,800 positions through

attrition; the cuts total nearly 30% of WaMu's employees. Included in

the purchase price was $1.5B of real estate or other assets (JPM's 10K,

12/31/08, p 82) and WMB's credit card business.

JPM's 10K, 12/31/08

http://www.secinfo.com/dsvr4.s3xf.htm#1stPage

Listed figures are as of 06/30/08 as stated in the OTS fact

sheet below.

http://files.ots.treas.gov/73002.pdf

WMB's credit card business had been expanded on June 6, 2005 with the

purchase of Providian Financial for $6.45B. JPM assumed both the WMB and

Providian credit card subsidiaries along with all other subsidiaries of

the bank. $10.6 Billion in credit card receivables were included.

http://en.wikipedia.org/wiki/Providian

JPM's Loan Portfolio

JPM stated in their conference call on 09/25/08 that the transaction would

be, "Accretive immediately, 50 cents" (per share), and that

it would result in a "Net cost savings (of) $1.5B, conservatively."

"$176B (of) home loans (were) assumed", with "$30.7B losses

projected."

http://wamucoup.com/JPM_telecon_all.wma

"Just shy of $300B of assets" were assumed, with net assets

of $31B after deducting liabilities. JPM then stated they would mark down

$31B related to the loans. Coincidence? JPM can use those write downs

to offset $31B in profits, resulting in a significant tax savings. At

a 35% tax rate, (general business tax rate) this represents a tax savings

of approximately $10.85 Billion.

When asked about loan losses if the economy were to worsen, JPM stated

that even under the pessimistic assumption if the loan losses exceeded

expectations, the worst they would do would be to end up flat. Why? Due

to the fact that the other WMB assets would still be making money. JPM

stated, "This transaction's generating $12B of capital over the next

3 years.” (That is after taxes.) The WMB acquisition would result in,

a "stable, predictable earnings stream" due to retail customers.

JPMorgan Chase acquired the banking

operations of Washington Mutual Bank for $1.9 billion. The fair value

of the net assets acquired exceeded the purchase price which resulted

in negative goodwill. In accordance with SFAS 141, non-financial assets

that are not held-for-sale were written down against that negative goodwill.

(Negative goodwill is a positive gain on a balance sheet due to gains

that cannot otherwise be accounted for.)

The negative goodwill that remained after writing down non-financial

assets was recognized as an extraordinary gain."

JPM

10K for 12/31/08; p 26, note (d)

http://www.secinfo.com/dsvr4.s3xf.htm#1stPage

“Effective

September 25,

2008, JPMorgan Chase acquired the banking operations of Washington

Mutual Bank for $1.9 billion. The fair value of the net assets acquired

exceeded the purchase price which resulted in negative goodwill. In accordance

with SFAS 141, non-financial assets that are not held-for-sale were written

down against that negative goodwill. The negative goodwill that remained

after writing down non-financial assets was recognized as an extraordinary

gain in 2008.”

After writing down part of the negative goodwill, JPM recognized an extraordinary

gain of $1.9B. Without this extraordinary gain due to Washington Mutual,

JPM would have reported a loss for the quarter.

FDIC accounting report on receivership detailing assets transferred

http://wmish.com/docs/WaMuReceivershipFinancialStatements(unaudited)thru123108.pdf

JPMorgans hedge fund was amazingly unscathed by the economic turmoil.

Good trading sense or is there more to it?

http://www.huffingtonpost.com/2009/03/03/jpmorgan-derivatives-5-bi_n_171312.html

So to sum it up, JPMorgan Chase acquired a massive

branch and credit card network that augmented their footprint in areas

where they were weak. For $1.9B, they acquired 2,239 branches in lucrative

markets that would have cost many billions to construct themselves. They

obtained an immediate $1.9B financial gain on the transaction, have a

future tax savings of $10.85 Billion, and expect to make an additional

$12 Billion in after tax profit over the next three years. And after that

they are left with a profitable bank that will continue to generate billions

of dollars of profits every year for the foreseeable future.

The question remains. Was this a fair auction? Did government regulators

do their jobs properly? Was Washington Mutual fairly compensated for its

bank?

Should Washington Mutual have been seized at all?

You be the judge.

Latest Developments and Links:

1. JP Morgan responsible for destruction of financial system:

http://www.marketoracle.co.uk/Article6826.html

2. WSJ FDIC memorandum:

http://online.wsj.com/public/resources/documents/wamu_memo.pdf

3. Geithner, Paulson named in $200 billion lawsuit

http://www.worldnetdaily.com/index.php?fa=PAGE.view&pageId=94539

4. -WAMU was in a lot worse shape in 2007:

http://wmish.com/docs/var/CAPITAL%20AND%20PROMPT%20CORRECTIVE%20ACTION%20RATIOS.doc

5. Feds say WAMU WAS the cause of collapse:

http://www.newyorkfed.org/research/conference/2009/cblt/interbank_market_HHH_jan09.pdf

7. JPM Shareholder Pamphlet::

8. WMI Documents:

9. Battle Brewing over Fire Sale of WaMu Banking Assets:

10 JPM Lawsuit against WMI:

http://amlawdaily.typepad.com/jp.pdf

11. NY Times Slams the OTS:

http://www.nytimes.com/2009/04/09/business/09views.html

Disclaimer: Click Here